As Trump Slashes Funding for State Disaster Planning and Response, the Bull's Eye in Danger Zones Keeps Growing

A big reinsurer offers yet another warning about mega-losses from hurricanes and the rest.

It sure seems that President Trump is setting himself up for a Bush-style “Brownie, you’re doing a great job” moment with his disastrous approach to the Federal Emergency Management Agency (not to mention NOAA).

Please read the new post below by

on a fresh warning from reinsurance giant Swiss Re about the potential for massive U.S. and global disaster losses this year. Crawford is a senior fellow in the Sustainability, Climate, and Geopolitics Program at the Carnegie Endowment for International Peace and her Moving Day Substack newsletter is a must.Here’s Crawford’s headline and deck, followed by a short excerpt. But you really should read the whole thing and subscribe to her newsletter!

Extraordinary coastal growth means 2025 could be a unthinkably expensive disaster year

Swiss Re warns there's a 1-in-10 chance this could be a year of $300 billion in disaster payouts -- but we keep building sandcastles on the beach

I sure hope the headline registers with Trump and his team (maybe he can at least read a headline). They still seem more focused on defunding and dismantling FEMA rather than revamping it. Thomas Frank at E&E News’s Climate Wire just posted this unsurprising update: Trump quietly halts money for preventing disaster damage. Here’s the nut:

President Donald Trump stopped approving new allocations in early April from a federal program that has been a top funding source for protecting people and property from disasters since 1989. The Hazard Mitigation and Grant Program has been used to elevate or demolish flood-prone homes, install tornado-safe rooms and strengthen buildings in hurricane or earthquake zones….

The move is Trump’s latest step to cut federal disaster spending and weaken FEMA as he considers abolishing or shrinking the agency. On Monday, Trump named 13 members to a council he charged with reviewing the agency and recommending overhauls.

Trump’s spending halt from the hazard-mitigation program comes weeks after he canceled another multibillion-dollar FEMA grant program, raising concerns that states and localities will stop efforts to minimize damage from future disasters. FEMA’s mitigation programs have been widely praised for reducing long-term disaster costs.

Click back to my post from early April on the cancellation mentioned above - a particularly atrocious move.

Here’s Crawford’s problem statement:

For decades, we have been building homes, businesses, and infrastructure, all packed closely together and crammed with treasures. That "value accumulation" leads to very high claims when storms or flooding arrive.

That's why a report by reinsurance giant Swiss Re said earlier this week that insured losses from disasters are trending straight up. Hurricane Ian (2022) cost insurance companies a whopping $64 billion—even though tougher building rules had been put in place following the devastation caused by Hurricane Andrew in 1992. Between 1975 and 2022, the number of people setting up shop in Ian's path—Fort Myers, Cape Coral, and Punta Gorda FL—grew more than sixfold.

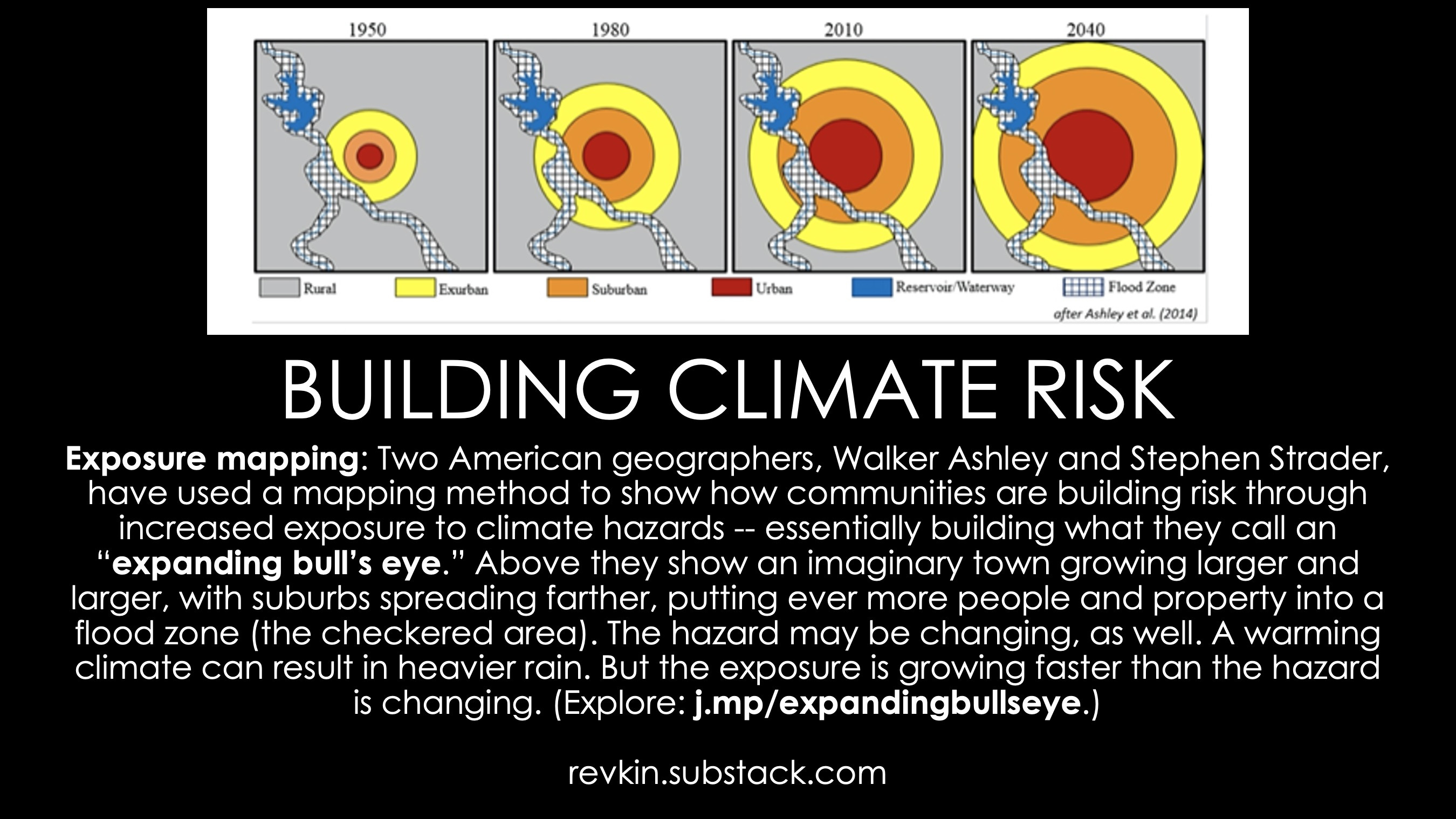

That’s the Stephen Strader / Walker Ashley #expandingbullseye of exposure to hazards that I’ve been writing on and speaking about since 2017.

Back to Crawford, here’s the solutions part of her post:

What's the right response? Swiss Re says the key is "coordinated efforts across stakeholders," which should include at least three things: (1) better building codes, although that's not a complete answer—remember Hurricane Ian, (2) improved zoning, so that we stop new development in floodplains and floodproof buildings that are already there; and (3) investment in safer infrastructure, which should include steadily decommissioning infrastructure that is unsafe.

In the abstract, and from a safe European distance, that all sounds simple enough. But even changing building codes at the local level in the US is astonishingly difficult.

Changing building codes is extraordinarily difficult, indeed, and then there’s the issue of exemptions for older buildings - whether the threat is flood or fire. See my post on the horrific losses in the Los Angeles fires for the importance of the word “grandfathered.”

A Wildfire Risk Watchword - "Grandfathered"

I’ll be posting more here soon on the Los Angeles-area firestorms extreme wind-driven fires [updated; see correction] and the implications of this continuing catastrophe for countless other communities. The firsthand accounts of those who’ve lost everything are intensely wrenching. They recall those I reported on in other such catastrophes. Do

What reinsurers should do

Finally, here’s Crawford’s admonition to reinsurers like Swiss Re to use their power to drive change in building codes, zoning and the other on-the-ground factors that are the top driver of losses in today’s hazard zones, let alone those coming with sea-level rise and warming:

Local governments often listen to the builders—we're in a housing crisis, after all—which means we are stuck with retrograde building codes and less-safe houses. We end up with a worse product that more people can buy, but that in the long term will experience devastating flooding. Modest elevation of houses in the 500-year floodplain would save millions, as would retreating from the current 100-year floodplain altogether.

So if Swiss Re really wants to ensure more insurable communities, they and their brethren will need to get involved in the building code world, conditioning the provision of re/insurance on adoption of humane standards when it comes to where and how we live. Someone with money has to make this move.

The back end of the Substack platform shows that hardly anyone clicks links. But I really do encourage you to click to her post and subscribe.

And of course please consider a financial chip-in to sustain Sustain What (I’m doing this for your sake):

While we’re at it, I hope you subscribe to

’s Disasterology newsletter and ’s Conflicted. I imagine most of you are already tracking ’s invaluable reality checking on disaster causes and claims.I’m closing this post with my faux Welcome Wagon guide for the 800-plus people moving to Florida every single day, most of whom have no real idea what they’re getting into. It was inspired by one of my Sustain What chats with my old friend and veteran Florida reporter Craig Pittman.